Your Medicare costs will depend on how much money you make

You may have heard that Medicare Part B will cost you more each month if you have a higher income, and this is true.

In fact, there are two Parts of Medicare – Part B and Part D – that are impacted by the Medicare Income Related Monthly Adjustment Amount also known as IRMAA.

Here’s how it all works.

Part B Premiums

Each year, the Centers for Medicare and Medicaid services (CMS), which is a branch of the Department of Health and Human services (HHS) sets the monthly premium amounts for Medicare Part B.

The Part B premium amount usually go up a little each year.

To give you an idea, when Medicare started back in 1965, the Part B premium was $3 per person, per month.

The base Part B premium for 2026 is $202.90 per person, per month.

When we discuss Medicare costs and plans, everything is an individual plan.

This means that if you are married, you don’t get to combine with your spouse for this number.

Each of you will have your own, separate premium.

This is true of all of your plans while on Medicare like supplement or advantage, drug plans, dental, vision, and others.

Calculating your Part B premium

When calculating your Part B premium, the Social Security Administration looks at your Modified Adjusted Gross Income from two years back.

It is 2026 as of the writing of this article.

To figure out my Part B premiums for 2026, they look back to my 2024 modified adjusted gross income from my 2024 tax return.

Next year, in 2027, there will be another 2-year look back, and they will use my 2025 tax return to determine my 2027 Part B premium amount.

This is important, because the number will change each year.

You are not locked into your income number from two years before you retire for the rest of your life. Your income amounts move with you.

This will be even more important later in this article.

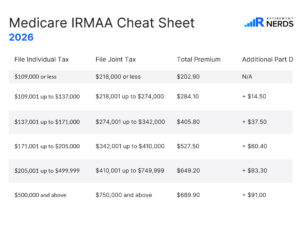

IRMAA Chart

The first two columns are Modified Adjusted Gross Income ranges.

The first column is if you file taxes individually.

The second column is if you file jointly with a spouse.

Remember, these are your numbers from your tax return two years ago.

The third column is your monthly Part B premium amount based on your income.

To clarify one more time – because we get asked this a lot – let’s say you are married, and you filed together, and your income from two years ago was $450,000.

Each of you, will have $649.20 per month as your Part B premium. Even if only one of you made all $450,000 and the other made $0 – or any combination of earning.

This means your combined household Part B premium amount would be $1,298.40 per month.

That is Part B, and there is also a similar bump in Part D premiums based on your income.

Part D

The last column on that chart shows the Part D surcharge.

Part D is your prescription drug coverage.

This surcharge gets added onto your regular Part D prescription drug plan monthly premium – if you have a standalone drug plan.

If you have a Medicare advantage plan that includes drug coverage at no charge, you would still see this Part D surcharge that you would be responsible to pay.

An example might help.

Part D Example

Let’s say my wife and I have a Part D plan and our monthly premiums are the average for the country right now at $34.50 per person, per month.

Our combined Modified Adjusted Gross Income – filing taxes jointly is that same $450,000 number from earlier.

My wife and I EACH need to add $83.30 per month to our Part D premium number, bringing each of our monthly premiums to $117.80 per person per month. Or, $235.60 per month as a household in Part D premiums.

Part B + Part D

The Part B and Part D combined premiums in this example for my wife and I would be $1,534 per month in premiums, just to have the plans, all based on our income two years ago. This number does not count any other plans we may have, like a supplement plan or dental plan or any others.

This usually prompts something like, “Hey, this isn’t fair. I was earning the highest income of my life two years before I retired, but I don’t earn near that much anymore because, well… I retired!”

Appealing your IRMAA

The good news is – you can appeal your IRMAA figure if your income situation has changed.

You need to submit what’s called an SSA-44 form and, based on certain life-changing events, you can get your premium reduced to either a lower level, or all the way back to the base level depending on your circumstances.

We have a video here that gives step-by-step instructions on filling out the SSA-44 form.

IRMAA’s impact on your retirement plan

If you own real estate, or business equity, or you want to pull out a bunch of money for a house remodel or to gift to a child… you need to be aware of these income levels.

Let’s say you’re 68 years old, you’ve been on Medicare for 3 years, and you and your spouse want to buy an RV, so you need to take out $100,000 from your investments or sell a property.

Well, two years later, when they do a two-year look back, you’re going to show a high income year, and your Part B and your Part D premiums could shoot up for that entire year. You may not remember the events from two years ago that contributed to a potential surprise increase in your Medicare premiums.

So, yes – IRMAA’s a big deal.

It can potentially make life a bit difficult for a year or two.

We help people with both Medicare and Social Security with a team of retirement nerds. The financial advisors watch this carefully and help people understand how their Social Security income, investment income, and other income sources all tie together with their tax burden and their Medicare premium amounts so you aren’t surprised and you can enjoy the retirement you want.