How to cover the gaps of Original Medicare

Most people have the tough decision between two different plan types that will cover many of the gaps Original Medicare leaves behind.

Those two options:

Medicare Advantage plans and Medicare Supplement – also known as Medigap plans.

Both cover the Original Medicare gaps, but they do so in different ways. This article will go over both options. Be sure to watch the video in this article for a more in-depth look.

Medicare Advantage

STRENGTHS & WEAKNESSES

If you ever hear about Medicare Part C – this is referring to Medicare Advantage plans.

Medicare Advantage plans replace your Government-sponsored, Original Medicare coverage. This means that the private insurance companies that offer Medicare Advantage plans take on all the risk and and handle all of the claims for your hospital and medical coverage. You will have 1 insurance card provided by the insurance company and you will not use your red, white, and blue Medicare card you received from Health & Human Services (HHS).

(Do Not throw away your Medicare card. Keep it safe. You just won’t need to show it while you have a Medicare Advantage plan)

The government pays these health insurance companies a monthly amount for each person on their Medicare Advantage plan.

Strengths:

Premiums

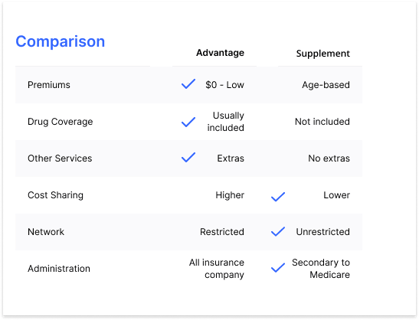

Advantage plans have low premiums. In fact, most are no-premium plans, meaning you have $0 premiums to have the plan.

Drug Coverage

Advantage plans typically include prescription drug coverage (Part D). A bit later, you’ll see that Supplement plans do not.

Other Services

Advantage plans often come with additional services like dental, vision, & hearing coverage as well as gym memberships and other perks bundled into the no-premium plan.

Weaknesses:

Cost Sharing

You will likely have higher cost sharing responsibilities with Medicare Advantage plans as compared with the most common Supplement plans.

Cost sharing refers to:

- Copays

A fixed dollar amount you pay each time you use the services associated with the copay.

Example: You visit a specialist and need to pay a $25 copay each time you visit. - Coinsurance

A percentage of the overall bill that you will be responsible to pay.

Example: You have a 20% coinsurance for chemotherapy. If it costs $1,000 for a treatment, you would pay $200.

In general (there are exceptions), Advantage plans will have more cost-sharing responsibility on you than Supplement plans.

Medicare Advantage plans have a Maximum Out Of Pocket (MOOP) where, if you reach this amount through paying copays and coinsurance, your plan will pay 100% of the rest of the costs.

Network

Advantage plans have specific provider networks connected with the insurance company or carrier you choose to work with. These networks are often strong in certain geographic areas, but weak in others.

All Benefits Through Carrier

All Advantage plan benefits are subject to the insurance company’s rules, exclusions, and processes. These will typically be less inclusive than a Supplement plan. Advantage plans are still regulated by Medicare, but the administration of the plans is managed by the insurance company.

This also means you could have a higher change of prior authorization or outright denial of certain treatments if the insurance company finds they are not medically necessary. We have a video on the prevalence of Advantage plan denials here: Advantage plan denial rates

Medicare Supplement aka Medigap

STRENGTHS & WEAKNESSES

The terms Medicare Supplement and Medigap mean the same thing. Medicare Supplement plans pay secondary to Original Medicare. This means that Medicare picks up the 80% coverage for Part B services and then sends the remaining 20% to the Supplement plan.

You will use your Medicare card provided to you by Health & Human Services (HHS) as well as an additional card provided to you by the insurance company you choose for your Supplement plan.

Strengths:

Cost Sharing

The most popular supplement plan (Plan G) has the Part B annual deductible that you would need to pay ($240 in 2024). Once that is met, you have zero medical cost sharing responsibility as long as the expense is covered and approved by Original Medicare.

No more copays or coinsurance, which is pretty great coverage.

Network

Supplement plans do not have a network. You can visit any provider, anywhere in the country as long as the provider participates with Medicare.

Pay Secondary to Medicare

Supplement plans pay secondary to Medicare. This means that if Medicare covers it, so does your supplement plan. No questions asked.

Supplement plan coverage policies, exclusions, and procedures align with Medicare, which are generally more inclusive than Advantage plans.

Weaknesses:

Premiums

The biggest weakness of Supplement plans would be their cost. The most common supplement plan premiums are called “attained age” plans. This means that as you attain a new age (get older) the more expensive you plan becomes.

There are other plan offerings that are not attained age plans, but instead are referred to as “issue age” – your rates are based on your age when the plan was first issued and “community rated” – your rates are based on the population in your surrounding community.

These plans types are less common than the attained age variety. Neither is better or worse than the other and each has its own advantages and disadvantages.

Typical Supplement plan premiums for the most popular plan (Plan G) range from around $100 per person, per month upwards of $300 per person, per month for a 65 year old, and go up from there.

Drug Coverage

Part D prescription drug coverage is not included with Supplement plans. This means that you would need to purchase a separate drug plan if you want drug coverage. These Part D plans have their own monthly costs, deductibles, copay, and coinsurance amounts you would be responsible to pay.

Other Services

Supplement plans do not come with the same additional services as Advantage plans. Bells and whistles like dental, vision, and hearing benefits will not be included with Supplement plans, and you would need to purchase each of those separately if you wanted that coverage.

Which is better?

Each has three check marks.

And that’s intentional.

The decision about which plan suits you best is a personal decision. Even between spouses, we often see one spouse get an Advantage plan and the other spouse get a Supplement plan. The decision is highly dependent on your situation and which of those six categories you feel carries the most weight.

In general, Advantage plans suit those who are healthier, with lower healthcare costs, and who do not plan on traveling outside their state or too far from their residential zip code. They typically have low to no drug costs and no chronic conditions. They also prefer lower monthly premiums, at times $0 depending on the carrier they choose and the individual’s geographic residence.

Supplement plans tend to cater to those who know that they will be utilizing the healthcare system often, know that they will travel often and don’t have to worry about a network, or prefer the peace of mind knowing that all hospital and medical costs are paid for once their deductible is met.

Wrapping it up

How you plan to cover the gaps left by Medicare is arguably one of the most important Medicare decisions you’ll make. We strongly recommend using an agent you trust who represents several different carriers so that you can work together with an expert and find the perfect plan for your budget, your health, and your peace of mind.

If you have someone like that in your life… use them. It does not cost you anything to use them. Your rates do not go up or down if you use them versus going directly to the insurance company themself. The difference is, an agent should know all of the intricacies of Medicare and help you avoid any mistakes.

If you don’t have someone like that in your life, we are happy to help however we can.